Here we go. The fed has officially broken something.

We witnessed the second- and third-largest bank collapses in history over the last few days.

A lot of regional and community banks are still under pressure. There could be more failures based on leverage on deposits.

But that’s not my focus today. A lot of people are expecting the Fed will NOT raise interest rates at all in March. They’re expecting a pause – even though inflation still remains hot in this economy.

Let’s take a bigger step back. A so-called “Pivot” in the market will not produce the Bull market rally so many people expect.

Why is this? History.

Let’s Check the Charts

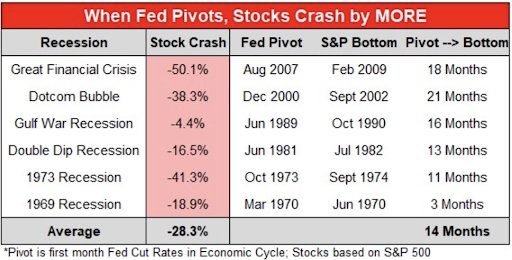

A friend of mine sent me this chart about three months ago. I should probably print it and keep it in my wallet next to a picture of my daughter.

Given the sheer number of questions I receive about the market on a daily basis, I’ll probably end up showing this chart more than her picture…

The Fed will eventually pivot, cut interest rates, and maybe increase its balance sheet all over again. This is how the system works. It’s built on cheap debt and a flimsy house of cards.

To prevent a total collapse, the Fed will eventually need to move back into the accommodation phase.

That said, we don’t tend to see a bottom at that time. Yes, we did bottom out in March 2020 once the Fed implemented a massive emergency printing regime. But that was not a pivot.

It was simply a response to the pandemic as the market was in a very bullish phase before the downturn.

In nearly every big crash before 2020… the pivot took months – and even more than a year – to find a bottom.

Today’s S&P 500 will likely follow this pattern of a selloff coming long after the Fed’s pivot. My expectation is that we’ll bottom out within nine to 12 months from the Fed’s pivot.

That said, it doesn’t appear we have reached this point just yet.

The sudden collapse of these two banks will force other banks to be far more conservative in the future.

We’ll likely see banks defensively hoard cash, take less risky loan portfolios, and increase demand for higher credit standards. This trend would be bearish for the economy, as fewer banks want exposure to credit risk. It reduces lending, which pulls money from the system.

Where to Focus Now?

We have a very serious crisis evolving in the banking sector right now.

Traders are slinging community and regional banks like they were trading meme stocks back in 2020. Quiet, conservative banks have become a primary target for day traders.

I think there will be a significant opportunity to buy banks on the cheap side, but it’s going to require patience in the months ahead.

The entire banking sector received a downgrade from Moody’s over worries linked to the economy and loans.

Even if the Fed does pivot, the damage has largely occurred. As a result, investors need to take a step back and understand the risks and opportunities for the future.

Tomorrow, I’ll be joining Don Yocham and Jeff Zananiri on a special Banking Crisis edition of “Roundtable LIVE” at 10am ET.

Yields are plunging at a rate that we haven’t seen since the 1987 crisis, the days after 9/11, or after the collapse of Lehman Brothers.

Tomorrow, we’ll discuss the probability of infinite Quantitative Easing, the likelihood of a Fed Put, and what to consider ahead of the Fed Open Market Committee meeting next week.

Bookmark your calendar for 10am ET tomorrow and join us at this link.

I’ll see you there.

To your wealth,

Garrett Baldwin

Market Momentum is Red

Momentum remains very negative despite today’s short-term pop. Markets were clearly oversold on Friday, and a short-term run seemed inevitable. We’re adequately hedged against a dramatic crisis over at Tactical Wealth Investor. To know what to buy now and how to focus on inflation-busting returns, go here.