The collapse of SVB Financial (SIVB) has sent the financial sector into a tailspin. I’ve only seen so many healthy banks take body blows once in my lifetime. That was 2008.

When our momentum reading went negative last week, I didn’t know that we’d have the second largest bank failure in U.S. history occur three days later. All I knew was that it went negative… and that we got out of the way.

We added a hedge with the Proshares S&P 500 ETF (SH) to our long-term portfolio, we took gains on Mosaic (MOS). We also secured a big win on Pangaea Solutions (PANL), which has been in a freefall from our stop. I sleep better at night by using my signal to eliminate my bias…

But there’s a lot of panic and a lot of fear in this environment.

And I want to address your concerns right now.

Something Broke. Now What?

The SVB Financial collapse is the “thing” that the Fed broke.

But did the Fed really break it?

It depends on how you define the person cracking the eggs. SVB’s financial conditions were largely due to a classic maturity mismatch.

The company owned a significant amount of long-duration mortgage bonds at a time when its clients’ industry was experiencing the biggest drawdown in capital allocation in years.

A classic bank run ensued.

It’s bizarre to me that the bank’s investments – perhaps some of the most conservative and boring products on the planet in actually safe bonds – were the culprit.

But given the Fed’s aggressive rate hikes, the value of those bonds fell, and the bank’s net asset value was stressed when one looked at the value of the bonds.

This is another accounting scandal if we really unpack it. The banks don’t have to mark these bonds to market on their balance sheet.

So, you know that the bonds are underwater, and the bank knows that the bonds are under water, but it doesn’t show up in their share price because the balance sheet doesn’t include these assets.

Why banks are buying long-term duration bonds in a cash-intense business makes little sense. But here we are.

Whether it was the accounting scandals of the Enron years, or the Dodd-Frank rules that addressed the Lehman efforts to keep toxic assets off their balance sheet, we always end up in the same place.

The Fed creates perverse incentives… and the risk-takers find a work around. Then the moral hazard is exposed, and we have a dramatic effort to shore up the system.

Why? Because no one bothered to revisit the very things that have caused so many other crises: Leverage, liquidity, and balance sheet tricks.

What Happens Now

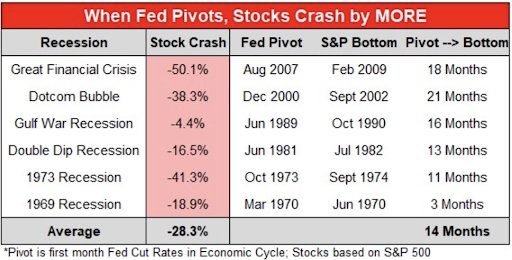

Unless the Fed just starts dumping money from the sky, I expect that economic conditions will tighten. But the Fed is in a very tight corner. To do so would invite much more inflation, and would rival the soft default on debt by the Bank of England in October.

Further tightening exposes an already weakening economy to greater liquidity challenges.

What’s so interesting about this situation is that it wasn’t a bailout of shareholders: It was a bailout of the entire banking system – and they’re about to realize that there is far more exposure than they thought over the weekend.

Everyone who is involved in this should lose their job, but we are not an accountable country. And we now have the people who created this crisis in charge of solving this crisis. It’s the same as it ever was.

With that said, if you have money in a bank don’t panic. You have deposit insurance for up to $250,000. If you have more than this in a bank, consider diversifying across various institutions.

We’ll likely see banks find ways to partner with other banks to swap excess deposits. Of course, that just points out the pointlessness of the entire FDIC system.

Meanwhile, as an investor, consider focusing on the long-term, and make sure that you follow my momentum writing so that you know when to hedge against downside.

I give you this reading for free, every day, and it has shown stunning accuracy at pinpointing when to buy and sell.

Again, it’s free. All you have to do is learn how to trade it.

The good news for Tactical Wealth Investor readers is that they already have a copy of my “Six Ways to Trade Negative Momentum” in their hands. Become a member right here.

To your wealth,

Garrett Baldwin

Market Momentum is Red

We’re well hedged, and we traded this very well from a long-term investor perspective. I’m not worried about the banks because the Fed will always backstop the economy. Do you honestly believe that we would have another Depression? No, we’ll just drop money out of the sky like always. But if you want to know where to put your money, you need to focus on the next 18 to 24 months. It all starts with our value and income plays over at Tactical Wealth Investor.