Amazon announced this week it will cut up to 10,000 employees.

That’s not a surprise… The e-commerce giant is the latest tech titan to announce sharp cuts to protect its balance sheet. Amazon.com Inc. (Nasdaq: AMZN) joins the ranks of Meta Platforms Inc. (Nasdaq: META), Carvana Co. (NYSE: CVNA), Peloton Interactive Inc. (Nasdaq: PTON) and more that have slashed employee rolls.

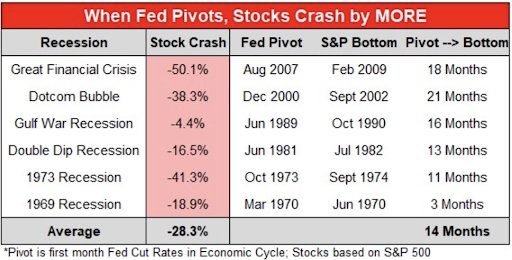

The news isn’t surprising. In an era of rising interest rates, recession expectations and chatter about “Fed pivots,” Amazon’s cuts are part of a bigger movement that could drive many technology stocks even lower in 2023.

Let’s dive in…

Cutting to the Bone

In October, a PowerPoint from Amazon’s leadership leaked to the media.

It outlined a dramatic shift in the company’s corporate strategy. Andy Jassy, who became CEO in 2021, started cutting costs, preserving cash and aiming to reallocate CAPEX toward boosting the stock value. It feels a little late for those initiatives…

Here’s an incredible number… Despite evidence that Amazon is growing, the company has a net asset value of minus $15.19. It also has nearly $80 billion in accounts payable on its balance sheet, which is money it owes suppliers.

Net equity is $138 billion… Long-term liabilities are about $140 billion.

This company needs to cut even more spending, and get its longer-term balance sheet in better health. Otherwise, things could get much worse in 2023.

But Amazon might actually be a redemption story. Elsewhere in the tech, software and cybersecurity sectors, a significant amount of pain is likely in the year ahead.

Daggers in Silicon Valley

I’ve long followed the weekly broadcast by Venture Capital managers Chamath Palihapitiya, Jason Calacanis, David Sacks and David Friedberg.

Two weeks ago, they discussed the state of Silicon Valley companies and why more job cuts are coming. More importantly, they outlined why a wealth of unprofitable tech firms are about to take a beating.

Two significant things are happening in Palo Alto…

The first is the longer-term trend of the Federal Reserve raising interest rates, and its impact on investor expectations. The Fed has pushed the risk-free rate on the 10-year bond higher, and increased the cost of capital for tech firms that might need to return to the market to raise money.

Simply put, their hurdle rate is going higher. That’s the amount of return they need to generate to justify their investors’ capital. Palihapitiya says the dollar in front of you is now far more important than the dollar down the road.

If the Fed funds rate increases to 5%, Silicon Valley firms must generate a “minimum of 500 basis points” above that level. That puts new pressure on companies to produce returns now.

And this reprioritizes the need for short-term profits.

“It’s way better to grow at 20% and be profitable than to grow at 100% and burn money,” Palihapitiya said.

The consensus of the hosts is that the tech sector is pivoting from growth to profitability. That puts a focus on “layoffs, cost reductions and cost savings,” David Friedberg said.

Investments in future growth are slashed while timelines for profitability scream forward.

Friedberg then pushes into the second driving factor: Elon Musk.

Based on what Friedberg has read, Musk could cut up to 50% of the employee base.

“It sets a new standard for how profitable a tech company can get,” he said.

With Musk cutting Twitter to the bone, it could be a standard where a lot of other companies do the same, and it pulls private equity outfits into the conversation.

That’s where the real fireworks start.

Because many growth tech companies might need to go private to survive… And if that’s the case, the valuations that private equity (PE) shops would be willing to pay are a pittance to valuations from last year.

That opens new wounds for company founders. It creates many problems for companies that are STILL carrying high valuations and aren’t turning a profit right now. Palihapitiya showed that the private universe of technology companies is in worse shape…

At a 10% to 11% hurdle rate, Palihapitiya notes, the companies on the left will need to engage in deep cuts to one day get to the right side of the chart.

Friedberg also notes that of the 200 public software companies on the right of the chart, a large number will “need to go private in order to do the restructuring that the market is

demanding that they do in order to get rightly valued.”

Palihapitiya also said PE deals will happen at “meaningfully lower levels” than the stock price when these companies went public or under the company’s final private round before its IPO.

He notes that roughly two-thirds of the companies that aren’t making money “have no line of sight” to profitability in the next two to three years — and most will need to raise future capital at “very egregious terms” to keep going as public companies.

Palihapitiya says 100 of those public software firms might end up as PE deals… which won’t be at favorable terms either.

Why?

Because — as he later explains — PE companies themselves can’t raise debt either given the current capital environment.

“So what do you think they do?” Palihapitiya said.

“They just pay 50% less than what they were willing to pay before because they have to pay 100% equity checks.”

Wow.

Checking In on Cathie Wood

I have long studied Cathie Wood’s ARK Innovation ETF (NYSE: ARKK).

Of the top 25 positions held by ARK Invest, just FOUR are profitable — 84% have a P/E ratio trading “At Loss.” From the broader sample of her largest publicly traded 96 holdings, just 34 are profitable.

So 64.6% of these companies are unprofitable… I will admit there are plenty of biotech stocks, but stick with the theme. On the tech side — in the larger portfolios — the fintech, software, communications, cybersecurity and other “innovators” are sprinting headfirst into a recession. Have they pivoted yet?

Have they awakened to the current environment and made the necessary changes and cuts?

Do they plan to? When?

I’d have to read a lot of 10-Ks.

But let’s look at just a handful of these names…

Remember that the lofty price-to-sales ratios of many tech companies were excused because the expectation of growth was high. Now, it should be a “forest fire” warning for companies that must cut costs to the bone just to survive.

Look at CRISPR Therapeutics AG (Nasdaq: CRSP), NVIDIA Corp. (Nasdaq: NVDA), Toast Inc. (NYSE: TOST), Bill.com Holdings Inc. (NYSE: BILL) and Cloudflare Inc. (NYSE: NET).

These companies are unprofitable, they have lofty valuations and they face incredible pressures to cut their employment count.

In addition, their executives aren’t buying their stock.

Why?

Because they likely expect their stock will move lower.

When momentum turns negative, it’ll be time to short these names again. I’ll show you the best way to do this on Thursday.

Enjoy your day,

Garrett